Snapchat has revealed its first efficiency report of 2025, exhibiting a gentle improve in customers, and improved enterprise efficiency, because of its efforts to raised have interaction SMBs.

Although issues stay about its constrained development, which means that Snap might have reached saturation level in its key markets, which means that it now must give attention to capitalizing on the eye that it has in these income segments to maximise its enterprise alternatives.

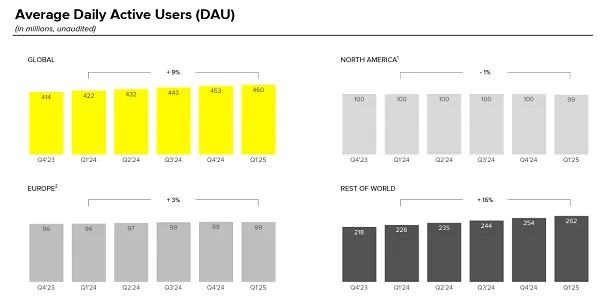

First off, Snapchat reached 460 million every day actives, a rise of 38 million year-over-year, whereas it’s additionally hit a brand new milestone of 900 million month-to-month lively customers.

The truth that Snap is closing in on a billion MAU is important, although as you may see, all of Snap’s development is coming within the “Remainder of the World” section, with the platform truly shedding viewers within the U.S.

That factors to future alternatives in growing markets, and underlines the continuing recognition of Snap, which does have a better churn fee as youthful customers age-up.

But it surely stays a broader concern for the app’s enterprise prospects, provided that Snap makes all of its cash within the U.S. and EU.

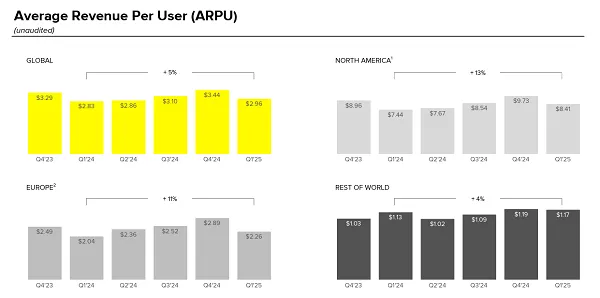

As you may see in these charts, Snap’s common income per consumer is method decrease in Europe than it’s in America, and method decrease once more within the “Remainder of World” section.

Snap’s seen vital development in India, as connectivity evolves in that market, and once more, that does bode nicely for future potential. However as Snap notes, its lack of development in its major consumer markets implies that it has to get higher at monetizing what it has, versus counting on development for income affect.

“We proceed to see sturdy development in our international group pushed by ongoing adoption of visible communication in much less mature markets. To proceed to develop our group in North America and Europe, we’re prioritizing innovation in three key areas: enhancing our core product worth of visible communication, investing in our AI and ML fashions for higher content material rating and personalization, and strengthening our creator ecosystem.”

That’ll stay a priority for market analysts, that Snap, whereas it stays well-liked, can be restricted in its key viewers bases, in income phrases. That’s why Snap’s been placing a much bigger give attention to new advert alternatives, with updates like its Affiliate Program, which incentivizes Snap customers to assist drive advert gross sales.

Basically, Snap’s development is spectacular, and it’s worthy of notice. But it surely must both speed up its enterprise improvement in rising markets, or present that it has the potential to squeeze extra income out of what’s more and more trying like a constrained core income base.

Which it’s doing. On the income facet, Snap introduced in $1.36 billion in Q1, up 14% year-over-year.

It’s not a large enhance, however Snap is increasing its alternatives, regardless of, once more, that stagnant consumer base within the U.S. and EU.

Snap says that development in its direct response promoting options, and its continued give attention to SMBs, has helped to spice up its income consumption, whereas Snapchat+ additionally continues to see good take-up, serving to to drive extra revenue for the app.

Certainly, Snapchat+ is now closing in on 15 million subscribers, representing a 59% improve in take-up year-over-year.

Snapchat+ has been essentially the most profitable of the brand new wave of social subscription choices, beating out X Premium and Meta Verified by way of total take-up, and underlining Snapchat’s nous for viewers understanding, and offering options that its customers truly need (and pays for).

And that’s offered a fine addition to Snap’s coffers:

“This helped contribute to Different Income rising 75% year-over-year to achieve $152 million in Q1 at a simply over $600M annualized run fee.”

It’s a lesser income ingredient, total, but it surely’s provided one other alternative for Snap to maximise its consumption in its key markets, and will turn out to be a much bigger focus on this respect.

When it comes to engagement, Snap cays that global time spent watching content material elevated year-over-year in Q1, which it believes displays its evolving AI and machine studying fashions for higher content material rating and personalization.

“To additional deepen content material engagement, we applied more energizing, extra responsive machine studying fashions, doubling the tempo at which they combine new tendencies and consumer interplay indicators. Whereas we anticipate that it’ll take a number of quarters to achieve our final aim of close to real-time mannequin refreshes, we’re inspired by the outcomes now we have achieved to-date.”

Additionally, as with each social app, brief kind video is working, with views on Highlight movies lower than 24 hours outdated doubling year-over-year.

That’s additionally serving to Snap improve its enchantment with rising creators, by making certain extra consideration and attain within the app.

Which is one other ingredient of focus:

“Over the previous 12 months, we onboarded hundreds of creators to our Snap Star program, driving sturdy momentum, with the variety of Highlight posts by Snap Stars rising greater than 125% year-over-year in North America in Q1.”

Extra influencer-originated content material means extra engagement, and Snap will proceed to give attention to enhancing its income and publicity alternatives to maintain these customers posting within the app.

General, it’s one other blended report card for Snap. I imply, double-digit development, in powerful market situations, possible signifies sturdy efficiency both method, however the truth that Snap hasn’t been in a position to develop in its key income markets stays a black spot on an in any other case constructive story.

Perhaps Snap has reached its restrict, and possibly that’s not so unhealthy, however it should imply that app’s enterprise prospects are additionally restricted alongside the identical parameters. Except it injects extra advertisements, which dangers turning individuals off.

Or its guess on AR glasses truly pays off, which, given competitors from Meta, I extremely doubt.

Both method, it’s what I’d name a mean report card from Snap, which reveals that engagement is growing, which may very well be of worth for entrepreneurs.